If you’ve been searching for a personal loan or home loan, you’ll have seen that along with the interest rate, lenders also display a comparison rate. But what is it? In a nutshell, it could help you identify the cost of a loan and easily compare it with others.

What is a comparison rate?

Lenders in Australia must legally display a comparison rate for all their loan products where a loan repayment is required (excludes Credit Card and Line of Credit products). Comparison rates for product types of Home Loans and Personal Loans are all calculated using the same formula, and are regulated by the National Credit Code. If you are looking for the best deal on your home loan or personal loan, then you should pay attention to the comparison rate.

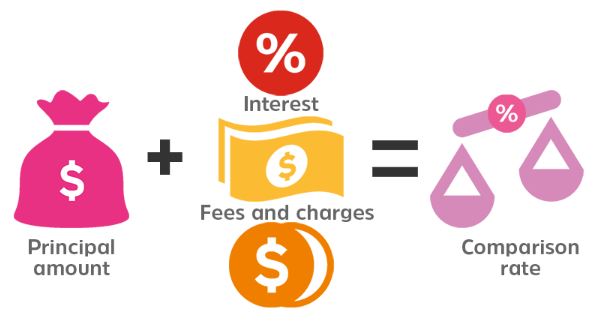

It can be a bit confusing initially, but just remember that the interest rate is the percentage that will be used to calculate and charge you interest each month, on the balance of the loan. The comparison rate takes into account any fees or charges incurred on the loan and represents the overall cost across the loan period. This means you shouldn’t just be looking at the interest rate, although a low one is great!

If you will be required to pay additional fees or legal charges, they have all been accounted for in the calculation of the comparison rate. If the comparison rate is the same as the interest rate, it most likely means there are no fees associated with that specific home loan.

|

Interest rate |

Comparison rate |

|---|---|

| The cost of borrowing the principal amount only. | The cost of borrowing the principal amount plus fees and charges. |

| Set by the bank or lender, influenced by the Reserve Bank of Australia (RBA) cash rate. | Often higher than the interest rate. |

| A short-term view of the loan cost. | A longer-term view of the loan cost. |

How is the comparison rate calculated on a home loan?

The comparison rate of a home loan is calculated with a standard formula using a loan amount of $150,000 to be repaid over a 25-year term and assumes both principal and interest repayments will be made.

The formula then takes into account the loan interest rate, upfront and ongoing fees, discharge fees and any low introductory rates and revert rates.

All of this is added together to come up with a total cost figure, and this is expressed as a percentage of the loan amount. A comparison rate of 3% means that your out-of-pocket expense for the loan is approximately 3% of the amount you're borrowing.

Is the comparison rate reliable?

Although the comparison rates of home loans and personal loans are all calculated using the same method, when you are deciding between two different loans you may not want to completely rely on the comparison rate alone.

Firstly, most home loans today are for much larger amounts than $150,000. They are also usually for the longer term length of 30 years (if not more).

Secondly, there are some fees and charges that don’t get accounted for in the comparison rate formula. For example, redraw fees and early termination fees are not included, neither are government charges such as stamp duty.

Remember that the comparison rate is there to make it easier to compare the costs of loans only. It does not cover other benefits that a lender may offer you, such as an offset account or flexible payment options.

P&N Bank Home loans

We have a range of different home loans to suit all types of customers. Whether you are a first-time buyer, refinancing an existing loan or an investor, we have you covered. And thanks to no establishment fees (or monthly fees) on most of our loans, our comparison rates are low like our interest rates.

Find the home loan option to suit you and speak to one of our Lending Specialists today, or contact your broker.

P&N Bank Personal Loans

Whether you need a new car, a last-minute holiday or to consolidate your debts, we can help. Our personal loans have competitive interest rates, low fees and flexible repayment options. It is quick and easy to apply online and you’ll get a response within minutes.

Important information

Banking and Credit products issued by Police & Nurses Limited (P&N Bank).

Any advice does not take into account your objectives, financial situation or needs. Read the relevant terms and conditions, before downloading apps or acquiring any product, in considering and deciding whether it is right for you. The Target Market Determinations (TMDs) are available on our website or upon request.