An offset account can help you manage the amount of interest payable on your home loan, and it can also help you reach your savings goal. To help you understand the ins and outs of offset accounts, we’ve answered a few of the common questions we get asked.

What is an offset account?

An offset account is a transactional account linked to a home loan that reduces the amount of interest payable for the home loan. Interest is charged based on the difference between your loan balance and the balance of the offset account. Essentially, the more money in your offset account, the less interest you pay on your home loan.

It’s possible to get a 100% offset or a partial offset, so you should consider which would work best for you. With a partial offset, only a specified percentage of the offset account balance is used to reduce the loan interest, whereas with a 100% offset, every dollar offsets the full balance.

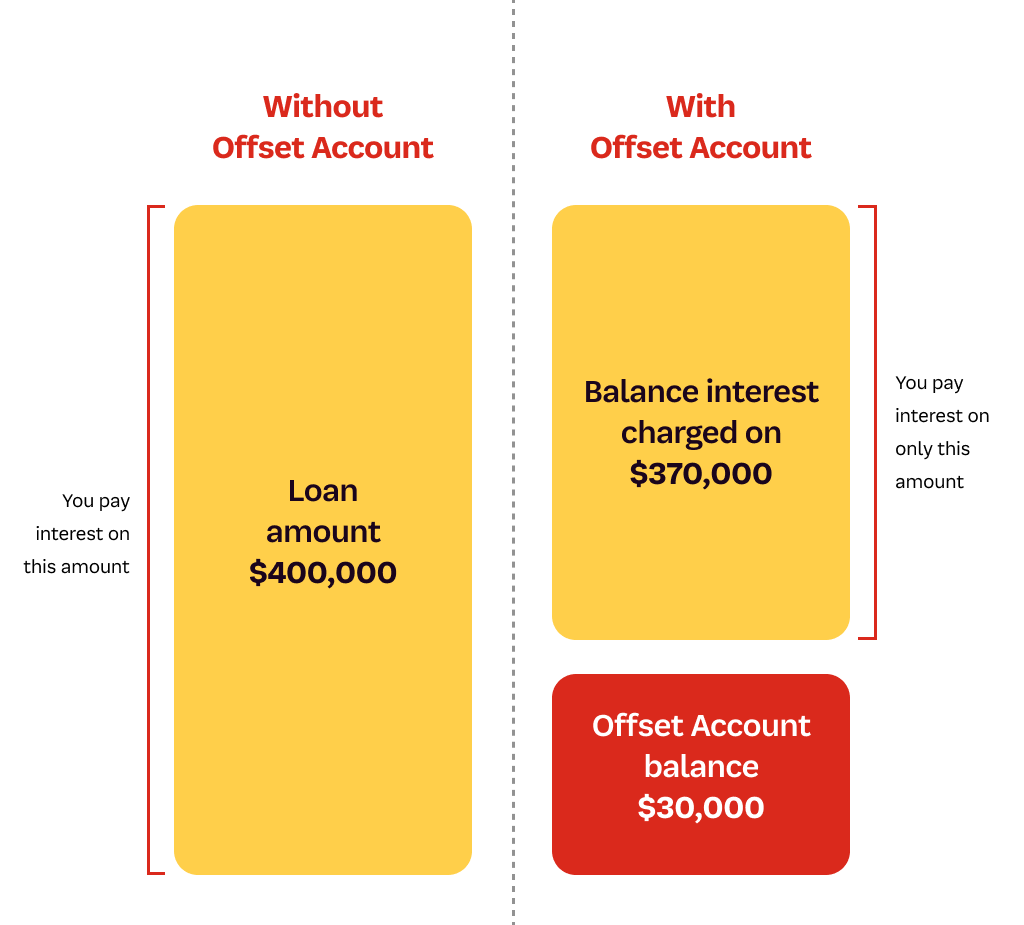

This image shows what a 100% offset balance of $30,000 would mean for a $400,000 home loan:

As you can see, interest would only be charged on $370,000 (400,000 – 30,000 = 370,000).

P&N Bank has a dedicated Offset Home Loan available for owner occupiers.

Why choose an offset account over a normal savings account?

Your home loan interest rate is likely higher than the rate your savings earn. By adding your savings into your offset account, you could be making your money work harder for you. Offset accounts are considered an effective way to minimise interest over the lifetime of your loan.

How can I make the most of my offset account?

It’s quite simple – the more you have in your offset account, the more you can reduce your home loan interest. A great way to boost your savings without having to lift a finger is to have your wage automatically deposited into your offset account. If you receive a lump sum payment or mid-year bonus, pop it straight into your offset account to boost the balance.

Remember, your offset account can be used like a savings account, and help you reach your saving goals.

What else can I do to maximise my offset account benefits?

Using a credit card with an interest free period for your monthly expenses can be a useful tool to help keep money in your offset account longer. By using your credit card to make purchases during the month, your money can keep working for you in your offset account by reducing the interest you pay on your home loan.

Make sure you choose a no or low-fee credit card option and clear the balance on the card once a month by the due date to avoid any interest being charged (cash advances excluded). Check out our article on how the credit card interest free period works to make sure you don’t get charged interest.

What should you look for in an offset account?

Not all offset accounts are created equal, so find the one that suits you and your financial situation. Consider things such as fees, withdrawal penalties, minimum balances and whether you can access the funds easily.

Questions to ask

You may also be interested in:

Join P&N Bank

Making extra home loan repayments, explained

Learn about what happens when you pay extra into your home loan account, the benefits of it, so you can take control of your future.

Local lenders

Important information

Banking and Credit products issued by Police & Nurses Limited (P&N Bank).

Any advice does not take into account your objectives, financial situation or needs. Read the relevant terms and conditions, before downloading apps or acquiring any product, in considering and deciding whether it is right for you. The Target Market Determinations (TMDs) are available on our website or upon request.